Slowing Growth Meets Persistent Inflation

Turning Heads

The First Quarter of 2026 did not fail to turn heads and raise eyebrows. From the Supreme Court ruling that struck down President Trump’s 2025 tariff plans, to the ongoing conflict in Iran, the American people remain visionless about the future. On April 7, 2026, Iran and the U.S. agreed to a conditional two-week ceasefire and opening of the Strait of Hormuz, a trade route that affects nearly 20% of global oil consumption. Q1 was defined by slowing demand and rising supply-side pressures, leading to weaker growth alongside persistent inflation.

Economic Growth (GDP)

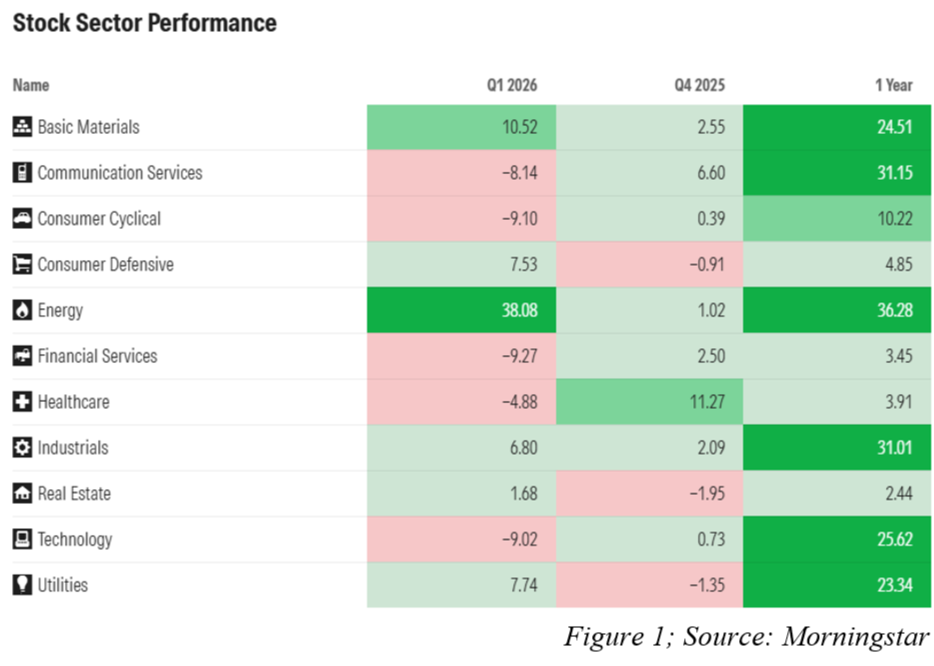

The Liquefied Natural Gas shutdown raises worries about the overall global economic health, not just oil. For example, helium is an integral part of semiconductor chip manufacturing, hurting Taiwan Semiconductor (TSMC), who source Big Tech’s chips. Though the conflict sent shockwaves to businesses, the energy sector flourished in Q1, returning 38% on the quarter (see figure 1).

Moreover, in Q1, value stocks outperformed growth. Value stocks comprise sectors like industrials, healthcare, financials, energy, and consumer staples. The key distinctions between value and growth stocks are:

Cash flow now (value) vs. later (growth)

Low multiples (value) vs. higher multiples (growth)

Stable (value) vs. high growth, high volatility

Growth stocks carry speculative risk. Tech companies typically thrive off innovation, and investors will buy in before sales materialize. Until then, the value arises based on speculation. In contrast, Walmart, for example, operates on a more predictable business model: “we buy apples from Farmer Joe, and we sell apples to the local families.” This model provides a concrete depiction of where the cash flow is coming from. Consequently, value stocks are historically less volatile than growth stocks.

Labor Market

Though the labor market posted decent numbers in Q1, people must contextualize their outlook and temper expectations accordingly. Total nonfarm payroll employment increased by 178,000 in March, with job gains occurring in healthcare, construction, transportation, and warehousing.

In March, the unemployment rate was 4.3%, down from 4.4% in Q4 (Bureau of Labor Statistics). Typically, that is a positive sign to economists, but the rate fall is prompted by 396,000 people dropping out of the labor force. The labor force participation rate fell below 62% for the first time since the pandemic (Reuters). Until 2030, Deloitte Global Economist Michael Wolf forecasts net international immigration of 321,000 per year into the U.S., significantly lower than the 2.4 million reported in 2024 (Deloitte). With less net immigration flowing into the American labor market, growth and production slow. To review the full economic impact of lesser net immigration, read the following article published by Wall Street Mojo.

It is important to note that the March jobs report does not capture the impact of the Iran war on the labor force, as Fifth Third Commercial Bank chief U.S. Economist Bill Adams underscores. In addition, federal government employment continues to decline.

Price Levels

Inflation improved in 2025, and trended in the correct direction, until the onset of the Iran conflict. The Organization for Economic Cooperation and Development forecast CPI to post 4.2% increase for 2026, up from previous forecasts of 2.8%. In this case, the Strait of Hormuz conflict is an exogenous shock to an already-slowing economy, further pressuring output. With 20% of global oil supply cut off, that inevitably raises the price-per-barrel, due to supply-demand principles; scarcity increases value, especially in an oligopolistic market like oil.

Interest Rates & Liquidity

To correct the markets, the FED implements a tight monetary policy approach. Tightening monetary policy raises the cost of capital, meaning businesses and individuals will spend less; less construction, less buying machines, less inventory accumulation. Entering 2026, analysts predicted rate cuts and spurred economic growth; the script has now flipped, and the FED plans to control inflation. Consequently, the FED met March 18, 2026, deciding to hold the federal funds rate at 3.50-3.75%.

Conclusion

The conditional ceasefire agreement is still under deliberation, and the end of the conflict is unknown. It is not the first time a conflict has arisen, and it will not be the last. In fact, the U.S. economy, since 1970, has endured seven major economic conflicts: from the Iran conflict of the ‘70s where the price of oil quadrupled, the financial crisis of 2008, the COVID pandemic of 2020, Liberation Day of 2025, and now the Iran war this year. Investors and advisers must continue reinforcing the importance of diversification, especially during these environments. To mitigate downside, investing in international, small-cap, and value companies, investors can (potentially) safeguard against heavy market downturns. With high risk comes high reward, and Q1 showcased the ugly side of high-growth investing.

Akili Kelekele is as an Investment Analyst at Allen Trust Company. Akili is a Quantitative Economics graduate from Tufts University. Before joining Allen Trust Company, Akili worked as an Equity Research Associate for D.A. Davidson in New York City.

Disclosure: The information provided in this writing is for general informational purposes only and does not constitute financial advice from Allen Trust Company and Allen Capital Management. Readers are encouraged to consult with a qualified financial advisor to assess their individual circumstances and make informed decisions based on their specific situation.